March 2019 - The Bulls are Marching on

- Mar 11, 2019

- 4 min read

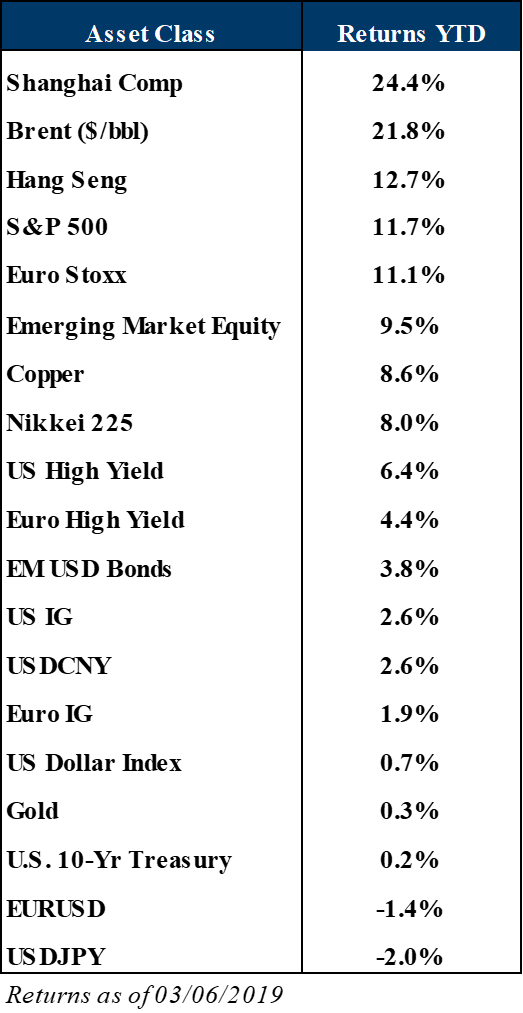

Risk assets continued their upward trend in February, following January’s surge. The MSCI All-Country World Index rose 2.9% on the month in local currency terms, bringing year-to-date gains to 10.2%. The main drivers of the market’s strength were the dovish policy stance by the Federal Reserve, significant progress on U.S. – China trade talks and improving business and consumer sentiment indicators. We think that equities won’t rise significantly from here, unless there are signs of stronger than expected corporate profits and economic growth. We expect volatility to rise again after dropping too much over the last two months.

U.S. equities slightly trailed developed market counterparts with the S&P 500 rising 3% compared with 3.2% for the MSCI World ex-USA index. More noticeably, the S&P 500 (+11.5% YTD) posted its best two-month start to a year since 1991. Positive performance during the first two months of the year typically bodes well for the year as a whole with an average annual return of 16.8% during such historical instances. On a sector basis, IT and industrials outperformed (+6.6% and +6.1% respectively) given their exposure to trade with China while consumer discretionary and communication services lagged (+0.6% and +0.8%). Since the market peaked in late September, sectors with positive returns are utilities (+8%) and real estate (+6%) while energy (-14%) and consumer discretionary (-8%) are still down. We view the U.S. equity market as fairly valued at the moment (forward P/E of 16.7x which is slightly above long-term averages) but remain overweight vs. other regions given the potential for stronger than expected corporate profits during the year. We prefer the financials and materials sectors.

In other developed market stocks, the Euro Stoxx 600 index rose 3.9% in February, bringing year-to-date gains to 10.4%. Top performers were from Ireland (6%), France (5%) and Italy (4.7%) while laggards were in Portugal (1.1%) and the UK (1.5%). European economic data is starting to show some signs of stability, with the Citigroup Eurozone Economic Surprise index rising over the last few weeks. In terms of monetary policy, the ECB is expected to announce another round of support for banks and encourage them to lend more, which would be marginally positive for growth. European equity P/E ratios remain relatively cheap (forward P/E of 13.6x) and the region is the most underweight among global investors. Although political uncertainty is high and economic activity is lackluster, we move our view to marketweight from underweight given a stronger likelihood for a soft/delayed Brexit and signs of stability in China.

Elsewhere, emerging market equities gained only 1% in local currency terms (0.1% in USD terms), dragged down by Brazil and Mexico (-4.4% and -4.2% in USD terms). Chinese stocks continued their recent surge, driven by progress on trade talks and MSCI’s decision to quadruple the weight of A-shares in its benchmark indices. The CSI 300 index, which tracks large companies listed in Shanghai and Shenzen, rose 14.6% on the month and YTD gains are now 30%. We expect inflows from foreign investors to continue to support the Chinese markets, and together with fair valuations (forward P/E of 11.5x) we expect continued outperformance. We also like Turkish equities as a tactical play given their cheap valuations (P/E of 7.2x) and signs of inflation coming down below 20%.

In fixed income, U.S. Treasury yields were relatively stable during the month and volatility as measured by the MOVE index continued to decline. The market continues to price in a small probability of one rate hike this year (10%), and the potential end of the Fed’s balance sheet normalization should anchor long-term yields. Together these two forces have driven the reach-for-yield across credit products.

US HY returned another 1.7% (6.4% YTD) and is off to its strongest start since 2001. Despite tightening 141 bps in two months, US HY spreads (at 390 bps) remain 75 bps wider than their tights in October and we see potential for further tightening absent any major shocks as technicals remain favourable. HY funds saw inflows of $6.2 bn in February and supply volumes were relatively strong at $21 bn. EUR HY outperformed US HY by delivering total returns of 1.9% (4.1% YTD) on the back of spreads tightening 52 bps to 391 bps. A delayed or soft Brexit should lead the EUR HY market to outperform the U.S. HY market.

US IG had a more muted month with spreads tightening 9 bps to 127 bps and returns of 0.4% (2.5% YTD). More cyclical sectors such as pipelines, metals and mining and industrial products outperformed (excess returns of 1.1-1.2%) while healthcare, retail and consumer products lagged (<0.3% excess returns). Technicals remain favorable with IG mutual funds seeing inflows of 1% of AUM in February while supply volumes of $106 bn were easily absorbed by the market. US IG spreads are currently trading wider than their post-crisis average and we expect them to stay stable in the next few months before potentially widening towards the end of the year. In Europe, IG spreads tightened 14 bps to 128 bps (total returns of 0.7%) and the average yield has dropped to 1% (from as high as 1.4% in late December).

In Emerging Market debt, hard currency sovereigns and corporates each returned 1% while local currency sovereigns returned -1.7% in $US terms. The latter’s returns were negatively impacted by the stronger $US (1.8% on average), particularly vs. the South African Rand (-5.9%) and Turkish Lira (-3.2%). EM debt funds have received inflows for 8 consecutive weeks, while supply volumes are running below last year’s levels. These positive technical factors and reach-for-yield should continue to support the asset class. Overall, we think the dovish stance by the Fed and progress on U.S.-China trade talks should continue to support risky assets, but given the speed of the rally it will require more positive catalysts to drive assets higher (such as stronger growth). We are a bit cautious about the sharp decline in cross-asset volatility which exhibits some signs of complacency. Low volatility can spur risk taking and carry trades but also end abruptly if there is a sudden shift in events. As always, risk-management combined with rigorous sector and geographical selection will remain key factors for investment performance. As usual, don’t hesitate to contact us to discuss our investment views or financial markets more generally.

Comments